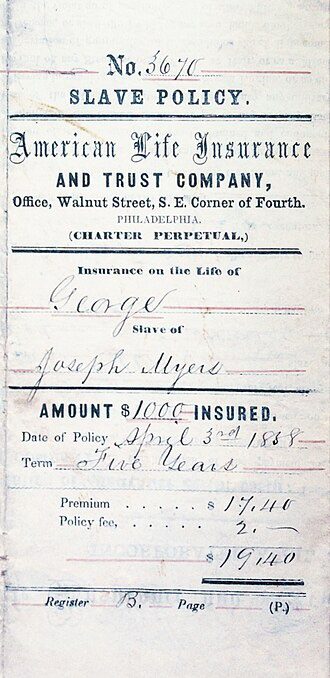

Slave-Era Insurance Policies

Slave-era insurance policies were financial instruments created in the 18th and 19th centuries to insure enslaved individuals. These policies treated people as property, compensating slaveholders for financial “losses” in cases of death, injury, or escape. Today, they provide essential insight into the financial underpinnings of slavery, genealogy, and modern reparations debates.

These policies illustrate how slavery was not only a social and political system but also a highly structured financial enterprise. By placing monetary value on human lives, insurance companies, banks, and courts reinforced the commodification of enslaved people and ensured that slavery remained deeply entwined with the nation’s economic growth. The surviving records of these policies now serve as both historical evidence of exploitation and as valuable resources for genealogists tracing family histories and communities seeking acknowledgment, justice, and repair.

State Registries & Locations

The states highlighted on this map represent locations where records of slave-era insurance policies have been identified. In some, such as California and Illinois, legislation required insurance companies to disclose policies connected to slavery. In others — including Virginia, Kentucky, Louisiana, and South Carolina — archival records reveal contracts held by banks and insurers covering enslaved workers in industries like agriculture, railroads, and shipping. Together, these state-level records demonstrate how widespread the practice was and how deeply embedded it became in both northern and southern financial systems.

Key Companies & Institutions Involved

“Logos shown for educational purposes only. All trademarks belong to their respective companies.”

Several major U.S. insurance companies participated in insuring enslaved people:

- ➡️ New York Life (Nautilus, 1845–1848): Paid ≈ $50,000 (~$1.7M today). Acknowledged in 2000.

- ➡️ Aetna (mid-1800s): Policies in KY & LA; used for loan collateral. Apologized in 2000.

- ➡️ Hartford Life (1830s–1865): Covered enslaved laborers in transport. Limited disclosure.

- ➡️ Mutual Life of New York (1843–1861, later Equitable): No formal apology.

Overview of Slave-Era Insurance Policies

Slave-era insurance policies reveal not only how enslaved people were commodified but also how deeply slavery was embedded in U.S. law, finance, and corporate systems. Below is a structured overview, with hyperlinks to explore details:

- ➡️ Origins & Context – Emerging in the late 1700s with the rise of plantation economies, these policies safeguarded slaveholders’ investments in agriculture, railroads, shipping, and mining.

- ➡️ Purpose – Policies treated enslaved individuals as insurable property. Coverage included deaths, labor injuries, and runaway losses.

- ➡️ Law & Economics – Courts upheld these contracts, and banks often required them as loan collateral. Enslaved people were appraised by age, gender, skills, and health.

- ➡️ Coverage Examples – Surviving documents show enslaved railroad workers, miners, and artisans insured at higher values, with occupational hazards listed in policy terms.

- ➡️ States & Companies – Policies were recorded across southern and border states. Major insurers included Aetna, New York Life, Hartford, Mutual Life of New York, Baltimore Life, and AIG.