Freedman’s Bank - Record Group (RG) 101)

The Freedman’s Savings and Trust Company, often called the Freedman’s Bank, was chartered by Congress on March 3, 1865, to serve newly emancipated African Americans and Black Union veterans. It grew rapidly to 37 branches across 17 states and Washington, D.C., with over 100,000 accounts opened during Reconstruction. Most deposits were small, typically under $60, but the records captured unusually rich family details that remain invaluable for genealogy. The bank collapsed in June 1874 after years of mismanagement and speculative investments, compounded by the Panic of 1873. Its failure devastated tens of thousands of depositors and seeded a long-lasting mistrust of banks in Black communities.

Purpose of the Freedman’s Savings Bank

The bank’s mission aligned with broader Reconstruction aims to stabilize families moving from enslavement to freedom. In practical terms, it sought to:

- ➡️ Provide a safe pslace to save wages and pensions.

- ➡️ Encourage thrift sand financial literacy through interest-bearing savings.

- ➡️ Enable asset-bsuilding (e.g., tools, livestock, land, homes).

- ➡️ Offer access neasr Black communities via a multi-state branch network.

- ➡️ Record family idsentities in depositor registers to safeguard heirs.

- ➡️ Channel soldiers’ pays (especially USCT into savings.

Operations

- ➡️ Headquarters: Washington, D.C.

- ➡️ Branches: At its peak, there were 37 branches across 17 states and the District of Columbia.

- ➡️ Depositors: Primarily freedmen, their families, and U.S. Colored Troops. Some poor white Southerners also used the bank.

- ➡️ Depositor Records: Records often included full names, family members, birthplaces, occupations, residences, and military service, making them invaluable for genealogy.

What the Records Contain

The registers are genealogical treasures. They often list:

- ➡️ Name of Master and Mistress

- ➡️ Full name, age, and place of birth

- ➡️ Current residence and occupation

- ➡️ Parents, spouse, children, and siblings

- ➡️ Military service details

- ➡️ Original signatures

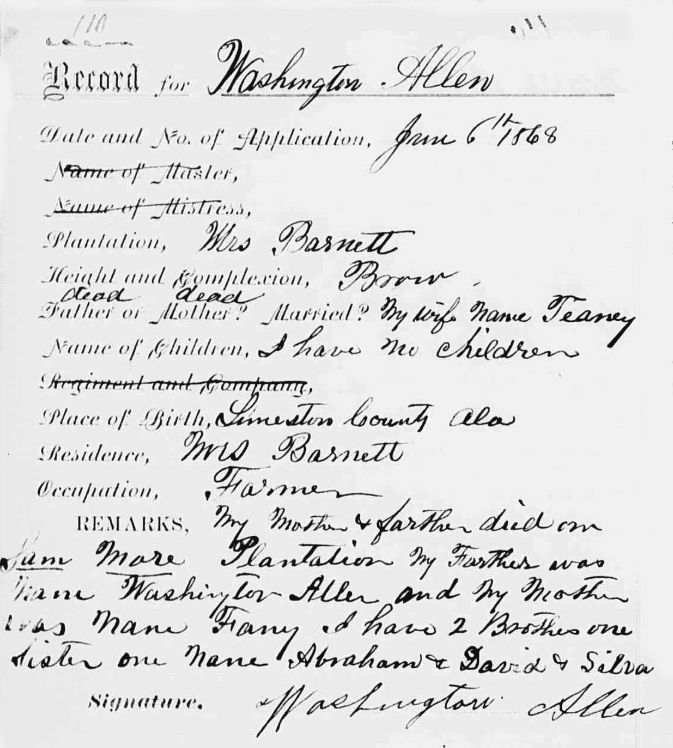

Sample of Bank Record

- Huntsville, Alabama

- Record for: Washington Allen

- Date and No. of Application: Jan 6th 1868

- Name of Master:

- Name of Mistress:

- Plantation: Wm. Barnett

- Height and Complexion: Brown

- Father or Mother: Dead / Dead

- Married? My wife name Teaney

- Name of Children: I have no children

- Place of Birth: Limestone County, Ala

- Residence: Wm. Barnett

- Occupation: Farmer

- Remarks: My Mother & Father died on Sam More Plantation. My Father was name Washington Allen and my Mother’s name Fanny. I have 2 Brothers one Sister one name Abraham & David & Silva.

- Signature: Washington Allen

Explore Freedman’s Savings and Trust Company Records by State

“Hover over a county or parish to see its name, Microfilm Publication, and a description of the records available. Each county/parish contains one or more markers showing the locations of Freedmen’s Bureau field offices. Click a marker to open that office’s records page, where you’ll find links, context, and research tips. You can also use the Select: dropdown menu above the map to jump directly to a county or parish.”

- Freedmen’s Bureau Field Offices (placed by county)

Who Could Deposit?

Although created primarily for African Americans, anyone could open an account. In practice, freedpeople, USCT soldiers and veterans. While some whites also deposited, the bank overwhelmingly reflected African American aspirations. (No dedicated Native American depositor program is documented.)

- ➡️ Freedmen and freedwomen seeking security for wages.

- ➡️ Black soldiers and veterans, many of whom deposited military pay.

- ➡️ Churches, schools, and benevolent societies.

- ➡️ Widows and orphans receiving pensions.

- ➡️ Black entrepreneurs and laborers across professions.

White financiers and connected firms benefited before the closing via access to speculative loans and insider networks; the losses were borne primarily by Black depositors and institutions. Scholars emphasize that the failure destroyed Black savings and trust, while real-estate and bond counterparties avoided equivalent losses.

What Was Lost

- ➡️ Depositors harmed: ~61,000 people.

- ➡️ Total lost: Nearly $3 million (1874 dollars).

- ➡️ Average loss per account: ~$49.

- ➡️ Recovery: At best, ~20% for those who filed claims.

- ➡️ Impact: Savings meant for land, homes, and taxes disappeared; churches and schools also suffered.